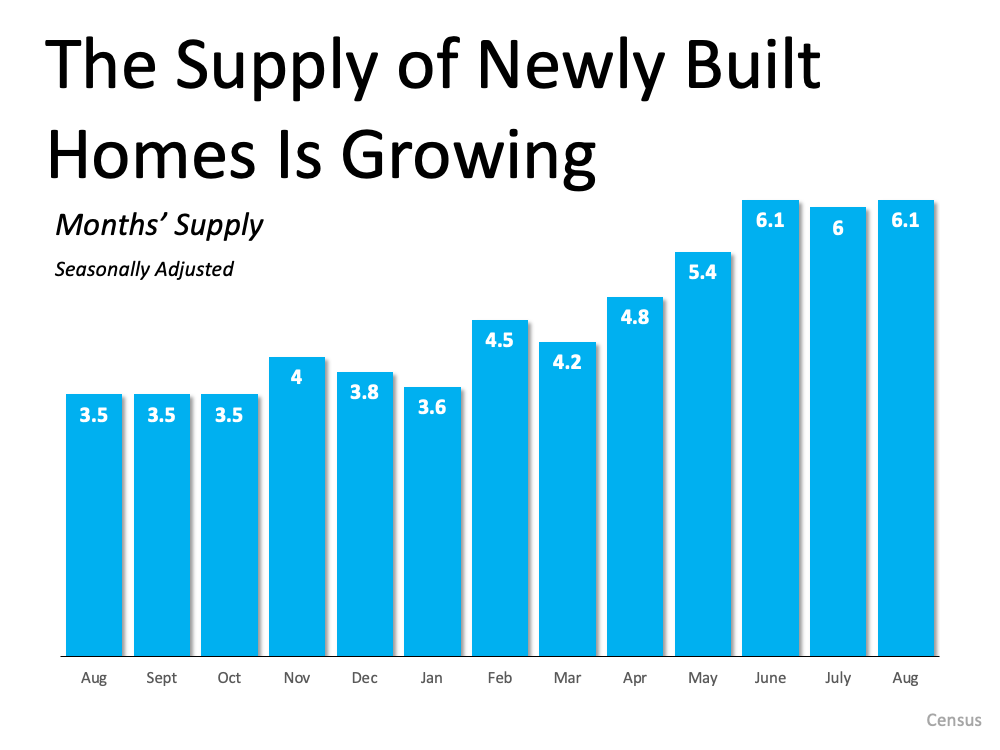

While today’s supply of homes for sale is still low, the number of newly built homes is increasing. If you’re ready to sell but have held off because you weren’t sure you’d be able to find a home to move into, newly built homes and those under construction can provide the options you’ve been waiting for.

The latest Census data shows the inventory of new homes is increasing this year (see graph below):With more new homes coming to the market, this means you’ll have more options to choose from if you’re ready to buy. Of course, if you do consider a newly built home, you’ll want to keep timing in mind. The supply shown in the graph above includes homes at various stages of the construction process – some are near completion while others may be months away.

“28% of new home inventory consists of homes that have not started construction, compared to 21% a year ago.”

Buying a home near completion is great if you’re ready to move. Alternatively, a home that has yet to break ground might benefit you if you’re ready to sell and you aren’t on a strict timeline. You’ll have an even greater opportunity to design your future home to suit your needs. No matter what, your trusted real estate advisor can help you find a home that works for you.

Bottom Line

If you want to take advantage of today’s sellers’ market, but you’re not sure if you’ll be able to find a home to move into, consider a newly built home. Let’s connect today so you have a trusted real estate advisor to guide you through the sale of your house and discuss your homebuying options.

Seller Question: Should I renovate my Albuquerque home before selling it?

(Transcript Snippet): “Tracy:

Sellers questions. They ask a lot. Should I renovate my house before I sell it? Tego?

Tego:

Yeah. That’s uh, that one comes up a lot and, and I think the, the answer, unfortunately, I’m going to take the cop-out answer is the answer depends. And the, the, the real answer is ask your realtor, ask your agent for advice, because it really is going to vary house to house to house. I will say, uh, just to make one broad statement is that major renovations usually do not pay for themselves, uh, if you’re going to do them and then just sell immediately for the most part, again, very generalized. It does not major renovations do not pay off. And when I’m saying major vendor renovations, I’m saying, you know, redoing the kitchen, redoing all the flooring, redoing stuff now, and I’m talking about, you know, updating stuff. Now renovations very different than taking care of deferred maintenance. That’s a different conversation, right? And so deferred maintenance is things like, um, your soffit in facia, you know, under your overhangs of your roof, you know, the paint is appealing and it looks dry and tired.

Tego:

Your roof, your roof shingles are worn out. Um, para pits are cracking, which we get a lot of times here in New Mexico. You know? So it’s, it’s the deferred maintenance stuff. Those things we’ll, we’ll, we’ll definitely distract from the sale of your house. Now, with that said, can I finish in today’s market right now? You know, we have such a low supply of homes on the market compared to the number of buyers, buyers. We have seen buyers, Tracy, and you can tell me if I’m right or wrong in this. We do see buyers, you know, maybe overlooking, you know, some condition issues with a property that maybe they didn’t five years ago.

Tracy:

I believe that’s true, but I would still say, if you have deferred maintenance, getting that taken care of before you put your house on the market is going to affect your sale price. And a lot of times buyers are going to ask it to be fixed once they go under contract on your house anyway. So it might be best to get the maximum dollar out of it, major renovations, um, you know, that’s what house slippers are doing, right? They’re trying to find a house that hasn’t been updated. That’s in a neighborhood that can justify a much better price if it gets updated, but still has plenty of room above what they’re going to spend. And they typically as a flipper, right? They have their go-to people, or they do the work themselves. They have trusted contractors and trusted resources. They do this all the time for us as realtors to recommend somebody to do 150,000 update on their house to get it sold is most, most sellers are just not able to even facilitate that, let alone,

Tego:

But many times it is possible. And in many times you will net more. It just really depends on where you’re starting. What is the condition of the home that you’re starting at? Cause that really is going to dictate if those remodels make sense or not.

Tracy:

I would say the best advice on the answer to this question, besides what you said and talk to your realtor and look at all of the implications are best thing you can do is just plan to really clean purge your house, get it staged properly and take care of the visual things, whether it’s smells, sights and what people are going to see when they see your house. And those are the things that most sellers are doing and make sense. Yeah.

Tego:

And, and, you know, merchandising it, you know, that’s gonna, you know, it’s going to net you the most when you’re getting ready to sell is have it cleaned beautiful, you know, and it, if it looks like a model home, you’re going to get the top dollar for.

If you’re looking to buy or sell a house, chances are you’ve heard talk about today’s rising home prices. And while this increase in home values is great news for sellers, you may be wondering what the future holds. Will prices continue to rise with time, or should you expect them to fall?

To answer that question, let’s first understand a few terms you may be hearing right now.

Appreciation is an increase in the value of an asset.

Depreciation is a decrease in the value of an asset.

Deceleration is when something happens at a slower pace.

It’s important to note home prices have increased, or appreciated, for 114 straight months. To find out if that trend may continue, look to the experts. Pulsenomics surveyed over 100 economists, investment strategists, and housing market analysts asking for their five-year projections. In terms of what lies ahead, experts say the market may see some slight deceleration, but not depreciation.

Here’s the forecast for the next few years:As the graph above shows, prices are expected to continue to rise, just not at the same pace we’ve seen over the last year. Over 100 experts agree, there is no expectation for price depreciation. As the arrows indicate, each number is an increase, which means prices will rise each year.

Bill McBride, author of the blog Calculated Risk, also expects deceleration, but not depreciation:

“My sense is the Case-Shiller National annual growth rate of 19.7% is probably close to a peak, and that year-over-year price increases will slow later this year.”

“. . . home price appreciation is on the cusp of flipping to a deceleratingtrend.”

A recent article from realtor.com indicates you should expect:

“. . . annual price increases will slow to a more normal level, . . .”

What Does This Deceleration Mean for You?

What experts are projecting for the years ahead is more in line with the historical norm for appreciation. According to data from Black Knight, the average annual appreciation from 1995-2020 is 4.1%. As you can see from the chart above, the expert forecasts are closer to that pace, which means you should see appreciation at a level that’s aligned with a more normal year.

If you’re a buyer, don’t expect a sudden or drastic drop in home prices – experts say it won’t happen. Instead, think about your homeownership goals and consider purchasing a home before prices rise further.

If you’re a seller, the continued home price appreciation is good news for the value of your house. Work with an agent to list your house for the right price based on market conditions.

Bottom Line

Experts expect price deceleration, not price depreciation over the coming years. Let’s connect to talk through what’s happening in the housing market today, where things are headed, and what it means for you.

Buyer Question: How much cash do you need to buy a home in the Albuquerque area?

(Transcript Snippet): “Tracy:

Question a buyer question of the week and a seller question the week. Want to get that in?

Tego:

So one of the most common questions, and I think, I think, let me, let me preface it this way. I think it’s the most common question that buyers don’t like, I’m embarrassed to ask maybe. And they don’t, you know, they don’t want to feel like they don’t know this answer because it feels like they should know. But the question, but the question is how much money, how much cash do I need to buy a home? How much money out of pocket is it going to take me to buy

Tracy:

How much money do I need to save before I talk about exact to a realtor about buying a home?

Tego:

The thing that’s interesting, there’s been a lot of surveys over the years that, you know, ask people and do they think how much do they think? And it’s, it’s interesting how many people think that they need at least 20% down to buy a home. Now, you know, there’s a whole debate is like, okay, should you, should you do 20% down? You know, or should you save up 20%? And a lot of people think you should, but, but that’s not what we’re talking about here. That what we’re talking about here is what does it actually take? Out-of-pocket so Tracy, for, for down payment, right? This is the amount of money you’re putting in toward the home to get your loan. What are, what are your options there?

Tracy:

So it could be anywhere from zero, okay. Up to whatever you want, right? No upper limit or you pay cash, right? So the V a veteran who qualifies for a VA loan, they have zero out of pocket loans for veterans. There may still be a few closing costs, but there are some options. So maybe the closing costs could be up to $3,000 depending on the price of the home. But it could be zero out of pocket.

Tego:

So far for that zero down program, it’s a dependent that it’s a veteran, right?

Tracy:

But he was served and left in good standing and qualifies to use the VA.

Tego:

And that’s the best program out there. The other zero down program that’s out there, that’s kind of not very well known is

Tracy:

The USDA loan. So this is for more rural areas to provide better financing options for people that are out of the metropolitan areas. So even some parts of Bernie, Leo, Placedus Edgewood, east mountains, south end, Valencia county, Sandoval county, different areas do qualify for a USDA zero down program. So there still could be some closing costs. So we’re talking about down payment is one portion of what it costs to buy.

Tego:

Well, let’s just finish up with the down payment conversation. So other than other than the zero down, we talked about USDA, VA, what other, what other down payment like tiers are there as we go through?

Tracy:

Sure. So then there’s the New Mexico mortgage finance authority that has a down payment assistance program that have to, um, qualify for, to have an income limit. And the limits are very high. I I’m surprised. So the mortgage finance authority, we call it the MFA.

Tego:

Oh, hi. What’s you’re saying though, is there’s a limit. So if somebody makes a million dollars a year, they’re not going to qualify for a down payment assistance program. Right. Right.

Tracy:

However, if it’s a two person household, you know, the income in, in Bernalillo county or Albuquerque, you can make up to, I think it’s about 70,000 a year and qualify for a down payment assistance program to help you get into a home.

Tego:

Um, and th those are great programs, $500 out of pocket, right.

Tracy:

And in Santa Fe, the limit is much higher, still like 80,000. And if it’s a three person family, it’s actually higher than that. So that’s a down payment assistance program which helps cover the closing costs. And the down payment, you have to have at least 500 out of your own pocket to put into it. There’s a couple different programs within the MFA, so it could be first home or next home. Okay. So if you have owned a home, there might still be a program for you. And first home is actually only having owned in three years. Not never been a homeowner. And then it goes to FHA.

Tego:

So let’s go to the next. So,

Tracy:

So then we’re at FHA, which is three and a half percent down payment. So let’s talk about a $300,000 house, right?

Tego:

Let’s talk about a $250,000 house. Cause I just did the math.

Tracy:

So down payment three and a half percent

Tego:

Is 87,

Tracy:

8,750. So when somebody says, how much down payment do I need to buy a $250,000 house, most people would be FHA financing.

Tego:

Well, okay. I’m going to contradict that because that’s actually not the most popular loan program right now. FHA is not actually conventional loans are more popular right now, but

Tracy:

So anyway, FHA

Tego:

FHA is a very popular, really good program, three and a half percent down. So next there’s actually these conventional loan programs

Tracy:

That might start at 3% down, 5%, 10%, 20%. So conventions.

Tego:

And in the, in the thing with those is you don’t have to know exactly what the best program for you is. You’re going to, you’re going to work with a mortgage lender, a mortgage broker, mortgage officer, whatever you wanna call it that is, you know, can look at your financial situation, look at how much money you’re able to put down and then, you know, gear the program and, and, and put the, put you in the best loan program for your situation. Right? I think that the takeaway we want to get here is that, you know, people can get into a home for, you know, $10,000 or less in down payment when they’re thinking about, okay, how much money do I need to save? Um, the next part of this conversation other than the down payment is the actual closing costs. So other than the down payment, which is your skin in the game, if you will, on equity in the house, right? What, what other costs is a buyer going to have getting to get into a home?

Tracy:

You’ve got the down payment and then you’ve got some other costs in today’s climate of being a home buyer. Typically the home buyers are paying for their own inspections. So that might be a home inspection for, let’s say around $350 give or take plus tax

Tego:

These days, aren’t they? Nope,

Tracy:

Three 50 is most of them, some of them are as high as five or more

Tego:

Plus tax,

Tracy:

A termite, dry rod inspection, you know, 80, 80 to $90. And, um, sometimes there’s a sewer line. Sometimes you’re looking at Wells and septics and things like that. So those are things to look at, but we have a whole chart of what things typically cost and who typically pays for them when you’re buying a house. And then there’s things like your first year of homeowner’s insurance, that’s paid up front at closing. So if you’re buying a $250,000 house, typically, you know, you’re going to get a quote from a home insurance company and maybe it’s 800 to $1,200. They’re going to collect that upfront for the first year.

Tego:

So I just wanna, I don’t wanna break this out here because I think it’s important distinction here when you buy a home, you know, let’s say, let’s say you’re buying a home with cash, right? You’re still going to have home inspections. You’re still going to have a termite or dry rot or any other inspections you want to have. You’re going to have those costs. You’re going to obviously pay for your, you know, pay for your insurance. Usually it’s a year in advance, but if you’re, if you’re getting a loan on the home, which we were just talking about, you’re going to have some, some expenses that are very specific to the loan. And so what would those be?

Tracy:

The loan fees. So to the lender, they’re going to charge a fee for underwriting. They’re going to charge a, an origination type fee, kind of a transaction fee. And, um, and there’ll be a few other fees, like a small one to check your credit and a couple of, um, mortgage endorsements. Because when you close on the home, they want to be on that loan as well as you at for ownership. But you know, those are, um, the lender fees vary a lot. So it’s really important. A lot of times people call a lender and they go, what’s your interest rate? And they’re trying to compare interest rates when choosing a lender. But what they don’t think about is how much does the lender also

Tego:

That is a big, big buyer tip, right? There is don’t just look at interest rate, look at the other expenses or other costs that a lender may be charging to do your loan.

Tracy:

So when you take both down-payment and other fees to buy a house, you can figure that, you know, the down payment is one portion and like Tigo just set on a lot of properties. It could be less than $10,000. And then the closing costs could be a couple thousand dollars depending on the price of the home and the types of inspections and what insurance costs and what the lender charges. So

Tego:

W you missed one, can I call you out the

Tracy:

Appraisal and the appraisal?

Tego:

Yeah. So the appraisal, you know, that, that is the, basically the, the valuation, uh, that has to be done by a third party for the bank, the lender that’s loaning you the money to buy this home, to verify that the value of the home is what it is, and that they’re making a safe loan on this property.

Tracy:

Basically, the praiser is basically the eyes and ears of the lender, right. Because the lender doesn’t actually go look at the house and they’re lending a lot of money. So they rely on an appraiser to say, yeah, you’re making a good loan. Yeah.

Tego:

Yeah. W one of the myths in our business, as the appraisers determine what a home is worth, no appraiser just verifies what the home is worth based on what the buyer’s willing to pay for it.

Tracy:

Right. So there you go. So if you’re wondering what, what kind of money you need to have saved to buy a home? There’s the quick thumbnail, but it’s always the best.

Tego:

Yeah. I hate to hear the long version, and these are the conversations you need to have with your realtor. If you’re, especially if you’re first time home buyer and, and, you know, really delve into these, and don’t be embarrassed to ask any of these questions. Right. You know, we don’t know. We know we don’t, if we don’t do something very often, we just don’t know. We do this every day.

Sellers have a great opportunity this season as buyer demand still heavily outweighs the current supply of homes for sale. According to the National Association of Realtors (NAR), today’s housing inventory sits at only a 2.6-month supply. To put that into perspective, a neutral market typically features a 6-month supply. That places today’s market firmly in the sellers’ market category.

That same NAR data also shows today’s inventory of single-family homes is trailing behind the level we saw last year (see graph below):Because of the ongoing supply challenges, buyers can feel like they’re wandering across a vast, empty desert when searching for their next home. That means your house could provide an oasis for buyers thirsty for options – and it could increase the chances of buyers entering a bidding war for your home.

The latest Realtors Confidence Index Survey from NAR shows houses are receiving an average of 3.8 offers. A multiple-offer scenario lets you select the best offer and gives you incredible leverage when you sell this fall.

Bottom Line

Buyers today are looking for relief as they wander today’s inventory desert. Listing your house this fall – before more options appear – gives your house the best chance to be noticed by multiple buyers. Let’s connect today so your house can stand out as the oasis it truly is.

With more new homes coming to the market, this means you’ll have more options to choose from if you’re ready to buy. Of course, if you do consider a newly built home, you’ll want to keep timing in mind. The supply shown in the graph above includes homes at various stages of the construction process – some are near completion while others may be months away.

With more new homes coming to the market, this means you’ll have more options to choose from if you’re ready to buy. Of course, if you do consider a newly built home, you’ll want to keep timing in mind. The supply shown in the graph above includes homes at various stages of the construction process – some are near completion while others may be months away.