Albuquerque home prices: 16% further growth by the end of next year

(Transcript Snippet): “Tego:

There was a story this week. I just want to hit on because it is at least in the news that, that I follow. Like, you know, you know how today, you know, in this world is we all follow our own news, right? We all get our news. We see what we want to see, but yeah, that’s a whole different, we don’t want to go down that road, but, but, um, I try to look at all these different points of view, especially when it comes to housing and real estate. But there was a story that came out that the, uh, the folks at Goldman Sachs, which, you know, they’re, they’re economist and looking at the economy and the market and everything that the headline was that, uh, home prices are going to grow a further 16% by the end of next year. So basically from third quarter this year. So it’s actually five quarters of what they’re talking about, but still it’s, it’s, uh, that’s a big increase over the next year. And in, uh, 63 months

Tracy:

And Goldman Sachs has a team of economists, and that’s where this story came from. So 16% growth between now and the end of 2022. That’s big. And we’re still

Tego:

Especially sorry to interrupt, but especially when you consider, you know, we’re, we’re probably gonna end this year somewhere between 15 and 20% price appreciation. And to be clear, we’re talking national numbers here. We’re not talking local, but, but still I think it, you know, it, it all applies. Right,

Tracy:

Right. So the supply chain issues, the, um, a number of people wanting to buy the lack of new homes being built and being affordable. When you think about the new homes being constructed in and around Albuquerque Los Lunas, Berlin, Edgewood, Santa Fe, Los Alamos, you know, the prices of those new homes, the entry level price now has gone up significantly in a year. Right.

Tego:

You know, it’s interesting because just maybe a year, let’s say two years ago, we were having this conversation about new construction in the Albuquerque area, new home construction, single family homes. And we’re saying, well, there’s just no such thing as a $250,000 house in Albuquerque anymore. That was only a couple of years ago. Now we’re saying there’s no such thing as a under $300,000 house in, in the greater Albuquerque area,

Tracy:

It’s changed significantly. We know that new homes, the newly constructed homes have a lot of really great features, including energy efficiencies, for comfort, for a cost to own, for the, you know, investment of them. There’s a lot of benefit from, for a new home, however, prices are up.

Tego:

Yeah, yeah. So, so anyway, that was an interesting story. So, you know, that went obviously, um, let’s say maybe triggered some people a little bit saying, what do you mean 16% more? Can’t can’t, you know, a homes are getting unaffordable, but it’s just, it’s an interesting, uh, thing. And I look at a bunch of different economists and they’re kind of all saying the same thing, Tracy.

Tracy:

They are, we’re still seeing it, you know, Tigo, if you think about what’s our average price right now, approximately somewhere, maybe

Tego:

Just, it’s just shy of 300,000. It’s been hovering right around 300,000 for the Metro Albuquerque area now.

Tracy:

So if you took a 16% on 300,000, let’s just look at what, um, what that might mean in price, right? A $300,000 house today. If we had 16% increase by the end of next year, that’s $348,000.

Tego:

Promising that though. We’re just saying, that’s what it is, what it is, right? I mean, yeah, that’s, that’s gaining wealth.

Tracy:

The takeaway is, you know, if you’re going to be buying in the next year, do it today. Even if it means locking in a new home to be built, lot of the new home builders are saying a house we’re going to start right now. Won’t even be ready till next may or June. Now, many of them have houses already kind of in the works that might be ready in February, March, April. I know there’s a few builders that are ready November, December with homes, but really good time to lock in home prices. If you’re thinking in the next year, you want to be a buyer and we’d love to talk to you about that. You know, we have a team of great realtors together

Tego:

And we really do. And if you want to reach out to us, it’s the Venturi Realty group with Keller Williams Realty phone number is four, four, eight eighty eight, eighty eight. And of course that’s in the 5 0 5 and our website is a welcome home. ABQ dot.

Tracy:

And I might say, if you like stats and you like to know about our housing market and follow that, I would say, follow Tigo on Twitter. He’s got great stuff. He posts out there. He’s kind of a Twitter freak. So

Tego:

Yeah, and I’ve, I’ve actually really in, Twitter’s kind of my, my social media of choice these days. Um, and, uh, you know, of course it all comes down to who you follow and who you don’t follow too. So you have to do that or you can get down and down in the weeds on certain things.

How much should you spend on your Albuquerque home?

(Transcript Snippet): “Tracy:

We had a question this week, how much should we spend on our house? And, you know, there’s lots of theories and lots of people who will weigh in on how much should we spend on our house. And there’s ways to look at it, right, as a percentage of income, um, or a multiple of next work net worth, or, um, household income, uh, comfort level of what you’re comfortable in spending, you know? So, so the, the whole thing let’s answer that question.

Tego:

There’s an old rule of thumb about, you know, your, your family budget. That’s, it’s a 50, 30, 20 rule. And what it says is that 50% of your income should be on your necessities, your housing, transportation, healthcare, food, you know, basically your, your basic necessities, right?

Tracy:

What’s the 30%

Tego:

30% are your, your wants your, you know, your extra, the dining out. Now I know a lot of people put dining out in food and they lump them together, but

Tracy:

That’s not really in that.

Tego:

Exactly. Yeah, I guess I don’t want to go down that road, but, but anyway, so dining out, travel entertainment, um, you know, special clothes, stuff like that.

Tracy:

So then the extra 20% to get to a hundred percent what’s that

Tego:

Savings and, you know, putting some money aside, every single paycheck, you know, people say it should be 10, this, in this case, it’s saying 20% should be set aside for retirement emergencies. You know, if you do the, the Dave Ramsey rule, you need that emergency

Tracy:

66 months of, um, of expenses

Tego:

She found. So, and, and, and it could, that could be debt repayment. So, so what they’re saying is 50% is your necessities. And part of that is your housing cost, either rent or a mortgage payment. If you’re more, you have a mortgage on a house. Um, historically Tracy housing costs have been somewhere in the 30% range of your, your income,

Tracy:

30% of your income. And, but lately with the low interest rates and higher home prices, what has happened with that?

Tego:

Well, the thing that’s interesting is that, you know, home prices over the last 10 years have been historically, um, let’s say affordable when you, when you figure the mortgage payment, because one, we had, you know, we had relatively low, uh, home prices, um, until this year

Tracy:

And low,

Tego:

Low appreciation. I mean, we really had very, very slow price appreciation since about 2012. It’s been very muted if you will. And we’ve had super low interest rates, you know, we talked about it’s funny, cause we say super low interest rates that, you know, at 4% and, and now we’ve, you know, we’ve been at this kind of 3% level for the longest time. So, so what’s happened is even a home prices have gone up a lot. Recently, the actual overall cost of your housing is still lower than historic levels just because the interest rates are so low and your payments are lower.

Tracy:

I know we’ve talked about this, like for years on this radio station that the, the cost of home ownership as a portion of your income is actually more affordable now than it was 20 years ago.

Tego:

Yeah, no, no, no doubt about that Tracy nets, for sure. So I just want to make one point here. So, so we talked about these rules of thumb, right? In, in, you know, what it costs or how much you should spend the problem with rules of thumb is they don’t take into account your personal circumstances. Right. Because when you’re thinking about buying a home versus maybe renting, you know, you’ve got to look at the math, right. That’s kind of what we’re talking about in people with brains like mine, we, we were all about the map, but it’s also emotion. It’s your circumstances, you know, what are the trade-offs that you’re willing to do and take?

Tracy:

So the, the bottom line here is we’re not going to give you a number, right. We need to just talk about it. Right? Okay. Let’s look at your total picture. Talk about what your comfort level is in a house payment, um, and, and come to something that makes sense, based on interest rates. We talk with the lender, we think of us, you and a lender as kind of like a trifecta triangle, right? The three of us work together unless you’re paying cash. And then, you know, you don’t really have a house payment, you have some taxes and insurance every year, but let’s talk about it, put together a plan of what makes you comfortable and then back into your home price.

Tego:

And so, Tracy, I’m going to just pull out some of these questions here. So this was, uh, Ben Carlson. He’s a financial advisor is, and he had written a piece on this. I do want to give him credit. And he said, it’s, you know, these are some of the questions that you should be thinking about when you’re saying, okay, how much should I spend on a home? Especially if you’re a first time buyer, should you stretch a little bit further? Maybe you’re going to stretch it a little bit further if you’re a first time home buyer.

Tracy:

Well, and if you’re in a, just starting a career where your income is going to go up quite a bit over the next couple of years, you might want to stretch and take advantage of that. Lowest,

Tego:

Do an adjustable rate mortgage, whatever you do. I don’t even think they really even exist.

Tracy:

Well, they’re not a better deal right now than a 30 year.

Tego:

All right. So these are some, I thought these, these were three really good questions was how long do I plan to live in this home? Um, could I see this being my forever home? Or am I going to just be here for a little bit and move on? And, and then, you know, how, how much am I comfortably spending on my housing? And then how do I compare that cost to, you know, whatever else I’m going to do to put a roof over my head versus rent versus buying. So I think they’re great questions at a very personal question and there’s no simple answer to it.

It’s impossible to research the subject of buying a home without coming across a headline declaring that the fall in home affordability is a crisis. However, when we add context to the most recent affordability statistics, we soon realize that, though homes are less affordable than they have been over the last few years, they are more affordable than they historically have been.

Black Knight, a premier provider of data and analytics for the mortgage industry, just released their latest Monthly Mortgage Monitor which includes a new analysis of the affordability situation. Here’s what the report reveals:

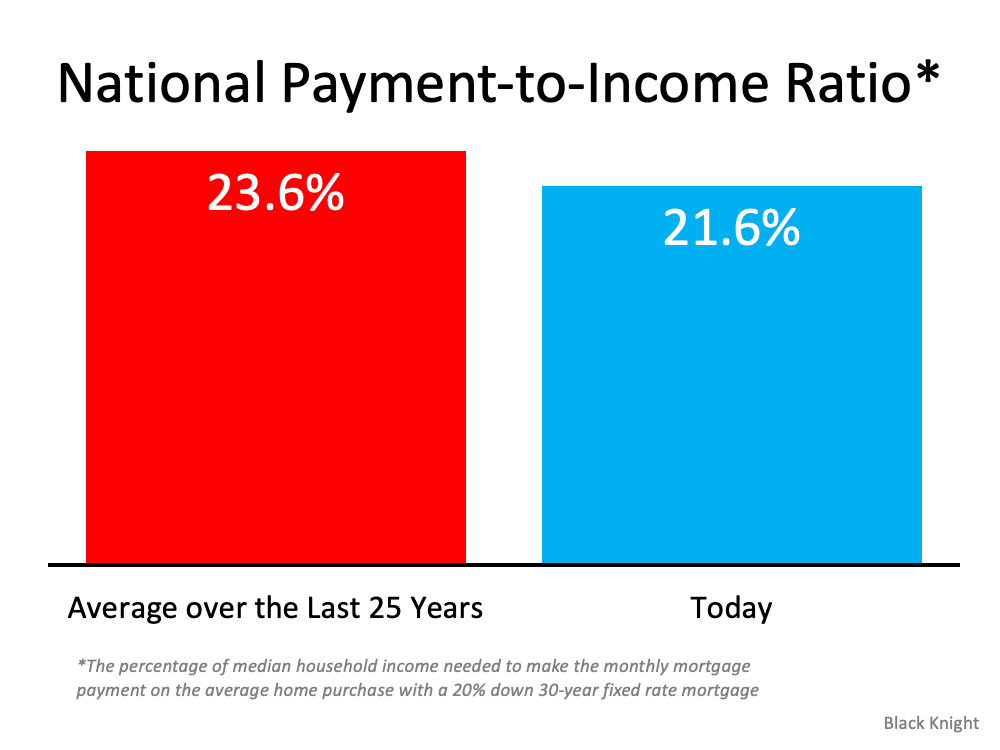

“The monthly payment required to purchase the average priced home with a 20% down 30-year fixed rate mortgage increased by nearly 20% (+$210) over the first nine months of 2021, . . . It now requires 21.6% of the median household income to make the monthly mortgage payment on the average home purchase, the least affordable housing has been since 30-year rates rose to nearly 5% back in late 2018.”

Basically, the report shows that homes are less affordable today than at any other time in the last three years. However, in a previous report earlier this year, Black Knight calculated that the percentage of the median household income to make the monthly mortgage payment on the average home purchase over the last 25 years was 23.6% (see graph below):Today’s payment-to-income ratio is more affordable than the average over the last 25 years. Given that context, we can see that American households still have the same ability to be homeowners as their parents did 20 years ago.

This confirms the recent analysis of ATTOM Data resources where Todd Teta, Chief Product and Technology Officer, explains:

“The typical median-priced home around the U.S. remains affordable to workers earning an average wage, despite prices that keep going through the roof. Super-low interests and rising pay continue to be the main reasons why.”

Bottom Line

It’s true that it’s less affordable to buy a home today than it has been the last few years. However, it’s more affordable to buy today than the average over the last 25 years. In other words, homes are less affordable, but they’re not unaffordable. That’s an important distinction.

The Truth: The Seasonality of Albuquerque’s Real Estate Market

(Transcript Snippet): “Tego:

One last thing I wanted to hit on Tracy is the seasonality of our market. Um, I know we’re just about out of time, but I wanted to just say there’s been a lot of conversations out there about, oh, the market is slowing down. There’s, you know, there’s more homes coming on the market. There’s um, you know, it’s well, let’s, let’s not put more into that. Yeah. Let’s not put the truth. It is not the truth. There’s been some national stories that, that show that, but here locally, Albuquerque, that’s not happening right now. We’re actually a hundred less homes in the market this week than just last week. So we’re actually declining in a number of homes in the market. We’re at historically low level of homes on the market. We still have strong buyer demand. And so, you know, the, the so-called slowdown that we’re seeing, um, even though it, it, it’s not the franticness that we had earlier in the year.

Tego:

Um, there’s still a lot of buyers out there and I’ll just say, one last thing is it’s very common that we do see a little bit less activity, a little less by buyer activity this time of year. It’s very common and there’s nothing unusual about it at all. Exactly. And so, you know, the people that are thinking, okay, here it comes, the market’s shifting. It’s like, no, this is, this is pretty much normal seasonal trends. Um, one thing I, you know, that, that we see year after year is that home prices tend to kind of peak out this time of year. What, what people are, what they’re selling for. They kind of, they kind of level off through the fall and into the winter and then usually go roaring back in the spring. So we’ll see if that, that historic trend stays.

![Your Home Equity Is Growing [INFOGRAPHIC]](https://files.simplifyingthemarket.com/wp-content/uploads/2021/10/18090947/20211022-KCM-Share-549x300.png)

![Your Home Equity Is Growing [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/10/18090949/20211022-MEM.png)