Home prices have increased significantly over the last year, which in turn has grown the net worth of homeowners. Appreciation and home equity are directly linked – as the value of a home increases, so does a homeowner’s equity. And with these recent gains, homeowners are witnessing their financial stability and well-being grow to record levels.

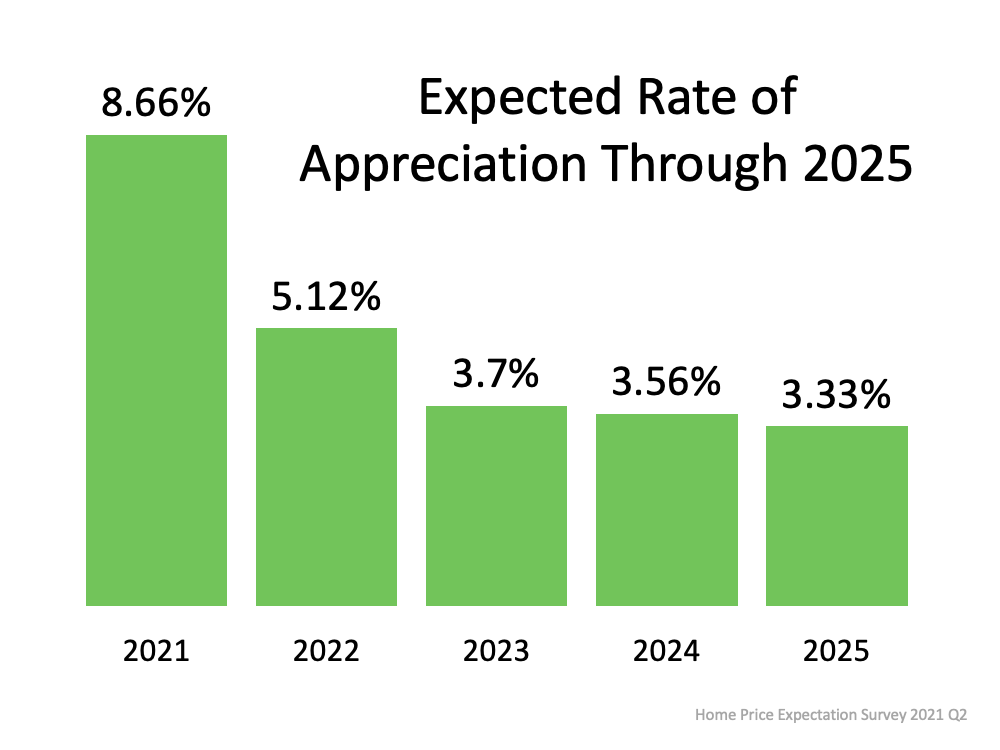

In more good news for homeowners, the most recent Home Price Expectations Survey – a survey of a national panel of over one hundred economists, real estate experts, and investment and market strategists – forecasts home prices will continue appreciating over the next five years, adding to the record amount of equity homeowners have already gained over the past year. Below are the expected year-over-year rates of home price appreciation from the report:

What Does This Mean for Homeowners?

Home prices are climbing today, and the data in the survey indicates they’ll continue to increase, but at rates that approach a more normal pace. Even still, the amount of household wealth a homeowner stands to earn going forward is substantial. This truly becomes clear when we consider a scenario using a median-priced home purchased in January of 2021 and the projected rate of appreciation on that home over the next five years. As the graph below illustrates, a homeowner could increase their net worth bya significant amount – over $93,000 dollars by 2026.

Home Price Appreciation and Home Equity

CoreLogic recently released their quarterly Homeowner Equity Insights Report, which tracks the year-over-year increases in equity. It shows an average annual gain of $33,400 per borrower over the past 12 months. In the report, Dr. Frank Nothaft, Chief Economist for CoreLogic, further explains:

“Double-digit home price growth in the past year has bolstered home equity to a record amount. The national CoreLogic Home Price Index recorded an 11.4% rise in the year through March 2021, leading to a $216,000 increase in the average amount of equity held by homeowners with a mortgage.”

The expected, sustained growth of home prices means homeowners can continue to build on the past year’s record levels of home equity – and their financial prosperity. It also presents today’s homeowners with a unique opportunity: using their growing equity for a home upgrade. With so few homes available to purchase and strong buyer demand, there may not be a better time to sell your current house and move into one that better meets your needs.

Bottom Line

Home prices are expected to continue appreciating over the next five years, and the associated equity gains are the quickest way homeowners can build household wealth. If you’re a current homeowner who’s ready to take advantage of your built-up equity, let’s connect today to discuss your options.

If you’re thinking of buying a home, there really is no time like the present. With today’s low mortgage rates, you have a great opportunity to get more home for your money. The challenge is inventory. Like you, many buyers want to capitalize on these market conditions, and it’s leading to more buyer competition and bidding wars.

If you’re having a hard time finding a home to buy, it may be time to talk to your trusted real estate advisor about a newly built home. Early indicators show new-home construction is beginning to ramp up. While new homes alone won’t be able to fix all of the inventory challenges, this does mean you’ll soon have more options as you search for a home. As a buyer, a newly built home may be exactly what you’re looking for – it’s brand new, and with builder customization options, it’s uniquely yours from the ground up.

Here’s what industry experts are saying about new homes coming to market:

Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), says recent research could indicate upward momentum when it comes to new home construction. Evangelou refers to the volume of new homes where construction began during a set period, known in the industry as housing starts.

According to that research, housing starts reached their highest level since 2006 in March of this year – an encouraging sign for the industry. While they dipped slightly in April, Evangelou reiterates that the level of housing construction is heading in a positive direction compared to recent years:

“…we are currently building 24% more homes than we typically have built in April in the last couple of decades. Thus, housing construction is trending upward with housing starts likely to reach 1.6 million for all of 2021 and rise further to 1.7 million in 2022.”

As new data pours in, it further confirms this trend. According to the latest Monthly New Residential Construction report from the U.S. Census Bureau, housing starts increased even more in May, which continues the ongoing upward trend (see graph below) and indicates that ground is being broken on even more new homes.Robert Dietz, Chief Economist and Senior Vice President of Economics and Housing Policy for the National Association of Home Builders (NAHB), singles out another encouraging sign:

“It is also worth noting that the number of single-family homes permitted but not started construction continued to increase in May, rising to 142,000 units.”

This insight that there’s also an uptick in single-family homes permitted serves as an additional sign that more new homes lie ahead. It’s important to realize that the construction doesn’t have to start on these homes before you may be able to purchase one. According to the Monthly New Residential Sales report from the U.S. Census Bureau, many new homes are selling before construction even begins (see graph below):These signs are all good news for housing inventory. And as the recent challenges of rising lumber prices and dwindling lumber supply begin to improve, builders will be able to increase their production even more in the months ahead.

Bottom Line

While the inventory challenges we’re facing today won’t be solved overnight, the increase in new-home construction means your house may have more competition in the market. Let’s connect to talk about finding your dream home and the newly built homes available in our area.

Cash Home Buyers & Equity: What the stats are saying

(Transcript Snippet): “Tracy: Speaking of cash offers, Tego. I was saying, we talked about this on the show, but I want to bring it up again because it keeps coming up. People keep saying, oh, there’s so many cash buyers and they’re just beating us out. And oh my gosh, all the cash buyers narrative. And, you know, we’ve, we were hearing that. And of course, you know what I did, Tracy, I know you went and did the stats, but you know, we, we, as a team have closed over 250 houses this year already. Right. And we’re going well, let’s look at it. And, and really, yeah, there are some cash buyers out there, but that is not different. Right. Do you have a stat for it? Tego: Yes, I do. And so what I looked at was I looked at the first half of this year versus, well, actually it was the first I say the first half, it was actually the first five months of 20 17, 20 18, 20 19 and 2020. And then of course, 2021, because I just went, it went through through may. Yeah. So it was five years back. And I was trying to say, okay, of all the homes that sold in each one of those years during that specific period, how many of them closed where cash, how many were conventional loans? How many were FHA loans? How many were real estate contracts, which is, you know, seller financing. And then how many of them were VA loans? And that’s, you know, those are the kind of the big, the five big buckets. And the thing that was shocking was it in 2021, that the number of cash buyers was actually less than 20 17, 18 and 19. Now last year, 2021, it was actually even lower. But this year it’s bumped up a little bit, but it’s, but it’s interesting because we hear these narratives out there where, oh, well, all these cash buyers are just coming in and they’re from California and they’re buying all our homes and they’re displacing us. It’s like, no, no, no. It’s, yes. There’s some of that. And we’ve always seen that. Right, Tracy. It, it, it didn’t just happen since last year that people from other states are coming here and buy Tracy: It. Right. And when we had our team meeting, we asked our team, there was about 20 some on, on the meeting, right. Where are people coming from? Are you seeing them coming from California? Is that the overwhelming? And it was like, everybody’s like, that’s just what people are saying. There’s no, there’s no facts behind that. And now it’s like, no, people are move up. They’re from here, they’re coming back here. They’re from all over there. They’re moving from one house to another, within the city. They’re, up-sizing, they’re downsizing. Tego: A lot of, you know, household formation is what we call it where we’re, you know, people that have maybe never been homeowners or, you know, maybe two, two people coming together to, to start a home and, and, and be the first-time purchaser. We are seeing a lot of first-time purchases, but most of those first-time purchases are people from, I mean, they’re from here, they’re not from elsewhere. So that was anyway. That’s a little myth busting there. https://welcomehomeabq.com Tracy & Tego Venturi Venturi Realty Group Keller Williams 1119 Alameda Blvd NW Albuquerque, NM 87114 (505) 448-8888 info@welcomehomeabq.com

Cash Home Buyers & Equity: What the stats are saying

(Transcript Snippet): ” Tracy:

Speaking of cash offers, Tego. I was saying, we talked about this on the show, but I want to bring it up again because it keeps coming up. People keep saying, oh, there’s so many cash buyers and they’re just beating us out. And oh my gosh, all the cash buyers narrative. And, you know, we’ve, we were hearing that. And of course, you know what I did, Tracy, I know you went and did the stats, but you know, we, we, as a team have closed over 250 houses this year already. Right. And we’re going well, let’s look at it. And, and really, yeah, there are some cash buyers out there, but that is not different. Right. Do you have a stat for it?

Tego:

Yes, I do. And so what I looked at was I looked at the first half of this year versus, well, actually it was the first I say the first half, it was actually the first five months of 20 17, 20 18, 20 19 and 2020. And then of course, 2021, because I just went, it went through through may. Yeah. So it was five years back. And I was trying to say, okay, of all the homes that sold in each one of those years during that specific period, how many of them closed where cash, how many were conventional loans? How many were FHA loans? How many were real estate contracts, which is, you know, seller financing. And then how many of them were VA loans? And that’s, you know, those are the kind of the big, the five big buckets. And the thing that was shocking was it in 2021, that the number of cash buyers was actually less than 20 17, 18 and 19. Now last year, 2021, it was actually even lower. But this year it’s bumped up a little bit, but it’s, but it’s interesting because we hear these narratives out there where, oh, well, all these cash buyers are just coming in and they’re from California and they’re buying all our homes and they’re displacing us. It’s like, no, no, no. It’s, yes. There’s some of that. And we’ve always seen that. Right, Tracy. It, it, it didn’t just happen since last year that people from other states are coming here and buy

Tracy:

It. Right. And when we had our team meeting, we asked our team, there was about 20 some on, on the meeting, right. Where are people coming from? Are you seeing them coming from California? Is that the overwhelming? And it was like, everybody’s like, that’s just what people are saying. There’s no, there’s no facts behind that. And now it’s like, no, people are move up. They’re from here, they’re coming back here. They’re from all over there. They’re moving from one house to another, within the city. They’re, up-sizing, they’re downsizing.

Tego:

A lot of, you know, household formation is what we call it where we’re, you know, people that have maybe never been homeowners or, you know, maybe two, two people coming together to, to start a home and, and, and be the first-time purchaser. We are seeing a lot of first-time purchases, but most of those first-time purchases are people from, I mean, they’re from here, they’re not from elsewhere. So that was anyway. That’s a little myth busting there. Cause

Tracy:

As for the stats, when people are throwing things around, I have my own Stat-O-Matic, so

Tego:

Conversation, I heard a conversation from a real estate training class where they were, people were just throwing data around and stats around and they had nothing to back it up. They were just saying stuff like, yeah, they’re all coming from, where does that? Where did you get that from? It’s like, well, that’s what I think. It’s like, well, anyway yeah, home equity that boy that is, that really hit the radar this week and all the economists that I follow re regarding real estate.

Tracy:

So let me just tell you, so we were meeting with the client last weekend. You and I, and talking about selling a house and anything and talking about where you can make money on your money. Right? We were saying, well, you could put it in and buy a CD or a treasury or this or that. And get, you know, right now they were advertising on a credit union last week when we were meeting that, if you wanted to put your money in for so many years, they were giving you extra. And it was going to be 0.4% interest, right? Could you imagine if the home equity was 0.4% interest? So when you think about wealth building and real estate this is where people build their wealth as a family. For the most part,

Tego:

It’s no doubt the number one wealth builder in the country, especially for the upper, or excuse me, the middle to lower class people. B because for the most part, people that are living paycheck to paycheck are not, they don’t have a 401k, they don’t have another savings plan, you know, but if you’re paying on your mortgage every month, you’re doing two things. One you’re paying down the principal every month and that’s forced savings. You’re also the, the equity in the home is growing over the longterm. Yes, we have ups and downs and there’s cycles and there’s going to be cycles and there’s always going to be cycles. I don’t think we’ll ever see a cycle. Like we saw from 2000, let’s say seven to 2010. I don’t think we’ll ever see a downturn like that. Again, there’s too many safeguards in place

Tracy:

Now. Well, do you think about when COVID hit or, you know, the stock market went down, but the value of my house didn’t right. Well,

Tego:

Values of homes have gone crazy in the last year. And so on the surface, you hear that and you go, oh, that’s, that’s a bubble, right. Well, okay. Is it, or is it not, let’s not go down that road, but, but for most part, most, not most just about any, you know, really reputable economists do not see a housing bubble, at least a price bubble. They do see an affordability bubble. That’s a different conversation, right? So anyway, but a couple of stats here average American, this is nationwide their equity, their home equity went up by $33,000 in the last 12 months in New Mexico. It’s $26,000. So you think about that, you know, every homeowner, if you just average it out in New Mexico that owned a home and there’s about a million homeowners in New Mexico, if you didn’t know that, I didn’t know that was a widow just shy of 2 million people, but there’s about a million homes in New Mexico. And that’s another stat I want to get to is how many of these people are finance and how many are free and clear.

Tracy:

It is an interesting number. How many people own their home outright.

Tego:

Outright. Yeah. Anyway, so, so and that’s, that’s figured into this average, right? So $26,000 gain in equity, but the number of people that, that have like, at least I think the number was the number of people nationwide that have at least 90, or excuse me I’m not, I’m not going to say this, right. There’s very few people that have less than 10% equity. Very, very few. It’s less than 10%. It’s very small.

Tracy:

I could see if somebody bought in the last year FHA with three and a half percent down. Yeah. That’s where that number is. Right. You know, if they bought three years ago, FHA with three and a half percent down, they have more than 10% equity. Yeah. Yeah. Yeah. And, and, and

Tego:

So one of the things that came up when I posted this on my, my Facebook is, well, how many people own their homes free and clear? And I thought, well, that’s a really,

Tracy:

And Claire is the term we throw around. Right. They own it out. Right. They have no mortgage on it, no mortgage. They own it.

Tego:

Yup. They own it. They don’t own anything to the bank on it or the own, you know, the bank doesn’t have a lien on it.

Tracy:

So what is the number? I want

Tego:

To say something, because I’ve heard this thrown around. It’s like, well, you have a mortgage, the bank owned your house. It’s like, no, the bank doesn’t own your house. You still own your house. It’s just that you have a loan from a bank or a lender that’s secured by your home. They don’t own your house. You still own your house. Anyway. I just, it’s one of those little things I see people say that just don’t make sense to me and it bugs me anyway. Okay.

Tracy:

So we’re all waiting on the number. I’m really in a mood today. Aren’t I? Yeah. How many people are owning their house outright, nationwide.

Tego:

42% of people own their home free and clear

Tracy:

And down the city block. And I see all these houses for four out of 10 houses on that street. They just own it. They don’t even owe a bank. Yup. That’s incredible. Isn’t it? Yeah. Yeah. And probably they’ve lived in that property a long time or a family member lived in that property that right. Especially

Tego:

Here in New Mexico. Right. We see a lot of that here, right. Yeah, for sure. For sure. Which

Tracy:

Is why people build wealth through home ownership. Right, right, right, right. And

Tego:

So, yeah, it it’s a, it’s a pretty oh, here’s the stat that I was talking about. Only 7% of people have less than 10% equity in their home. Very few numbers,

Tracy:

Very few numbers. Very, very few, very small. Wow. I don’t know too much coffee or I think

Tego:

It’s one or the other for sure. That, that goes to two. Well anyway, sorry, go ahead. You had something else you wanted to share.

Tracy:

Yeah, I’m good. I was, I was looking at the stats of the different types of loans that you had pulled up for us to see in front of us where you were saying the 17, 18, 19, 20, 21, the types of loans the different types, you know, VA FHA owner financing, you know, the biggest by far was conventional that’s our market. And so when we put a house, we, when we sell a house here in our multiple listing service, we then go in, when we close it and show it, we put in the, the details on it and we put in how it was sold type of financing or cash. Right. Yeah. And so you went back and figured out how to run those numbers. And by far conventional loans was the biggest and conventional is typically somebody with higher credit that might put more money down. Right. And then there was FHA and VA, which were much smaller. FHA tends to be maybe a first-time buyer, three and a half percent down. Yup. Right. VA obviously we really appreciate our veterans who are eligible for VA. That’s a zero down loan and it’s the best loan you can get. If you’re eligible. If you’ve done some military service and honorably discharged and qualify for it by far, it’s the best loan out there.