Running the numbers: The most expensive and the most affordable places in Albuquerque

(Transcript Snippet): “Tego: Um, anyway, so Tracy, um, we were talking about, you know, okay. These different parts of Albuquerque, I saw a national story. It was talking about, you know, what are the most expensive places in the country. Right. And I’m like, well, okay, well, let’s, you know, you, and I know this, but I bet people are curious, what are the most expensive parts of Albuquerque? You know, where are the most expensive homes? And we could also talk about where the most least expensive homes as well. And so, uh, I ran the numbers and I’m sure you probably know,

Tracy: I haven’t seen the numbers, but I could guess I know we always like that. So I’m going to say, well, most expensive, a couple things come to mind right. Far Northeast Corollas plus Cetus

Tego: Yep. Good Job

Tracy: So 87122, 87048

Tego: So 87122. If people aren’t familiar with it, that is the area that is basically north Albuquerque acres and San Diaz height, right? Yep. Um, the, uh, the next one is a 7 0 4 8, which

Tracy: Pirellis the next one is 043 Placidas

Tego: Placidas is next. Yep. And then, um, well, 043 and then 047, which is, uh, eastbound.

Tracy: Yeah, that’s north 14 up a ways. Not, not Cedar crest to Harris, but San park

Tego: And then 87008, which is a old town I believe now. Oh my gosh. Now I feel,

Tracy: I was going to say, oh

Tego: Wow. Now I found it really silly. Um, oh, oh, I’m sorry. That’s that’s Cedar crest. I’m sorry. That’s why. Yeah. Yeah. So it’s these mountains also. Um, and then, uh, yeah, so, um, and then ACM 059 also, um, uh, east mountains. Yup. Yup. And then 87111, which is what we consider the kind of a traditional far Northeast Heights, you know, that’s like Tatooine and in everything around there,

Tracy: Quavis school

Tego: District, north of Montgomery. Yeah, exactly. Yeah. So yeah, it’s, it’s pretty interesting. And then we get into the north valley, um, and, and, uh, just kind of on down the list then like 87114 which is the north west, you know, paradise Hills, uh, T uh, my, on that really tailored ranch, I guess, but mostly paradise Hills, some of the newer areas. So yeah, it’s interesting, you know, it, it definitely seems, and I, I think we see that, right. Tracy has, we’re, we’re looking around the city, you know, there are certain pockets where there’s some, you know, very expensive homes, north valley, um, far, far Northeast Heights, San Diego, San Diego, um, um, Sandia Heights, north Albuquerque acres. So yeah, very, very interesting. If we look at the most active, uh, uh, zip codes and know, you know, the most number as in the most sales, it’s interesting because

Tracy: This

Tego: Rio Rancho, yeah. This year, it was north Rio Rancho with, uh, over 1600 homes year to date through.

Tracy: Interesting. And second is, uh, 87120, which is, um, Southwest and a little bit over I, 40 west of

Tego: We’re still considered Northwest, but it’s just a one, two. Oh, oh, I’m thinking of one to one. Yeah. Yeah. Got it.

Tracy: Got it. Southwest and a little bit over I 40.

Tego: Yeah. So, and then 87144. So you think about, you know, the areas where there is a lot of homes, right?

Tracy: 114, yeah. Northwest and then south Rio Rancho. So yeah, so those are all very hot and in a lot of newer neighborhoods, you know, in the last 20 years in those areas.

Tego: Sure. And when we look at, you know, the, the buyer’s market versus sellers market, and, you know, what are the hottest zip codes in town? Uh, what we see are the zip codes of like 87120. And, you know, again, it’s these places where the prices are a little more moderate, right. Are going to be the, the, the most active you’re going to see the most competition for homes that come on the market. Right. Right.

Tracy: And of course, if you think of a pyramid right. Of, of our home prices, the highest price homes we’re going to are going to be the least amount of sales. Right. Right. And the ones that are most affordable, obviously there’ll be the most or bulk of the sales. So it only makes sense for, for sure. For sure. We don’t have to be like really smart to figure that out.

There are a lot of questions right now regarding the real estate market as we head into 2022. The forbearance program is coming to an end and mortgage rates are beginning to rise.

With all of this uncertainty, anyone with a megaphone – from the mainstream media to a lone blogger – has realized that bad news sells. Unfortunately, we’ll continue to see a rash of troublesome headlines over the next few months. To make sure you aren’t paralyzed by a headline, turn to reliable resources for a look at what to expect from the housing market next year.

There are already alarmist headlines starting to appear. Here are two recent topics you may have seen in the news.

1. Foreclosures Are Spiking Today

There are a number of headlines circulating that call out the rising foreclosures in today’s real estate market. Those stories focus on an overly narrow view on that topic: the current volume of foreclosures compared to 2020. They emphasize that we’re seeing far more foreclosures this year compared to last.

That seems rather daunting. However, though it’s true foreclosures have been up over the 2020 numbers, it’s important to realize that there were virtually no foreclosures last year because of the forbearance plan. If we compare this September to September of 2019 (the last normal year), foreclosures were down 70% according to ATTOM.

Even Rick Sharga, an Executive Vice President of the firm that issued the report referenced in the above article, says:

“As expected, now that the moratorium has been over for three months, foreclosure activity continues to increase. But it’s increasing at a slower rate, and it appears that most of the activity is primarily on vacant and abandoned properties, or loans in foreclosure prior to the pandemic.”

Homeowners who have been impacted by the pandemic are not generally the ones being burdened right now. That’s because the forbearance program has worked. Ali Haralson, President of Auction.com, explains that the program has done a remarkable job:

“The tsunami of foreclosures many feared in the early days of the pandemic has not materialized thanks in large part to the swift and decisive foreclosure protections put in place by government policymakers and the mortgage servicing industry.”

And the government is still making sure homeowners have every opportunity to stay in their homes. Rohit Chopra, the Director of the Consumer Financial Protection Bureau (CFPB), issued this statement just last week:

“Failures by mortgage servicers and regulators worsened the impact of the economic crisis a decade ago. Regulators have learned their lesson, and we will be scrutinizing servicers to ensure they are doing all they can to help homeowners and follow the law.”

2. Rising Mortgage Rates Will Slow the Housing Market

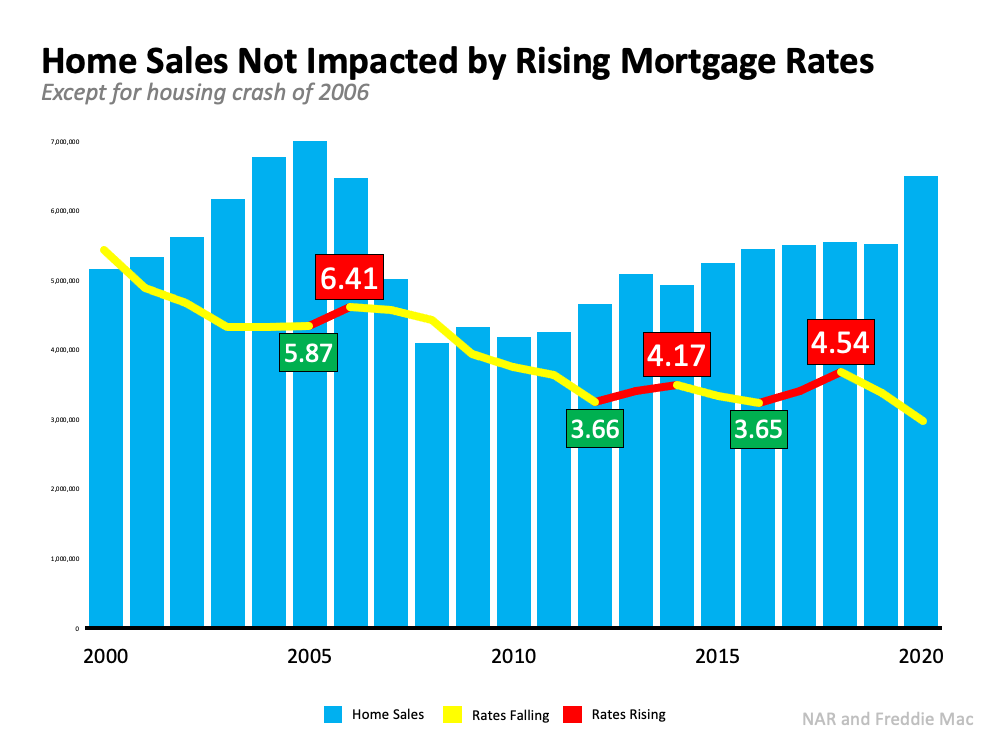

Another topic that’s generating frequent headlines is the rise in mortgage rates. Some people are expressing concern that rising rates will negatively impact the housing market by causing home sales to dramatically decline. The resulting headlines are raising unneeded alarm bells. To counteract those headlines, we need to take a look at what history tells us. Looking at data over the last 20 years, there’s no evidence that an increase in rates dramatically forces sales to come to a halt. Nor does home price appreciation come to a screeching stop. Let’s look at home sales first:The last three times rates increased (shown in the graph above in red), sales (depicted in blue in the graph) remained rather consistent. It’s true that sales fell rather dramatically from 2007 through 2010, but mortgage rates were also falling at the time. The next two instances showed no meaningful drop in sales.

Now, let’s take a look at home price appreciation (see graph below):Again, we see that a rise in rates didn’t cause prices to depreciate. Outside of the years following the crash, prices continued to appreciate, just at a slower rate.

Bottom Line

There’s a lot of misinformation out there. If you want the best advice on what’s happening in the current housing market, let’s connect.

Your equity is a powerful tool that can help you achieve your goals as a homeowner. And chances are, your equity grew substantially over the past year. According to the latest Equity Insights Report from CoreLogic, homeowners gained an average of $51,500 in equity over the past year.

If you’re looking for the best ways to use your growing equity, here are four options:

1. Use Your Equity To Buy a Home That Fits Your Needs

If you’re finding you no longer have the space you need, it might be time to move into a larger home. Or, it’s possible you have too much space and would like something smaller. No matter the situation, consider using your equity to power a move into a home that fits your changing lifestyle. Moving into a larger home can provide extra space for remote work or loved ones. Downsizing, on the other hand, may mean saving time and money by caring for a smaller home.

2. Move to the Location of Your Dreams

If the size of your home isn’t a challenge but your current location is, it could be time to relocate to a new area. Maybe you enjoy vacationing in the mountains, at the beach, or another area, and you’re dreaming of living there year-round. Or perhaps the distance between you and your loved ones is greater than you’d like, and you want to close the gap. No matter what, your home equity can fuel your move to the location where you really want to live.

3. Start a New Business

If you’re not ready to move into a new home, you can use your equity to invest in a new business venture. As the U.S. Small Business Administration Office of Advocacysays:

“There is an estimate of 31.7 million small business owners in the United States, many of them started their business with the equity they had in their home.”

While it’s not recommended that homeowners use their equity for unnecessary spending, leveraging your equity to start a business that you’re passionate about can potentially grow your nest egg further.

4. Fund an Education

Whether you have a loved one preparing to head off to college or you’re planning to go back to school yourself, the thought of paying for higher education can be daunting. In either situation, using a portion of your growing equity can help with those costs, so you can make an investment in someone’s future.

Bottom Line

Your equity can help you achieve your goals. If you’re unsure how much equity you have in your home, let’s connect today so you can start planning your next move.

When will we have more homes in the market? Looking at Albuquerque’s Real estate market data

(Transcript Snippet): “Tego:

So I did a little, uh, analysis here, Tracy. And, um,

Tracy:

When will we have more homes on the market to go? I know you were working on that analysis

Tego:

As I, I looked at a lot of different data. And so if, you know, if you’re not familiar with the pin going on in the Albuquerque real estate market, and by the way, this is Tico and Tracy Venturi with the Venturi Realty group of Keller Williams Realty in Albuquerque. And if people want to reach us trace,

Tracy:

Uh, best is just call us 448-8888 Of course, that’s in the (505) 448-8888 or welcomehomeabq.com.

Tego:

That’s great. Thank you. So, uh, you know, the, the, the real story of our market is just the limited number of homes on the market now, and that’s not just our market. I’m sorry. That’s, that’s nationally. That’s, that’s, I’m not going to say everywhere, but you know, most markets healthy, real estate markets have a, a much lower number of homes on the market than what would be considered healthy. And, and what’s what’s happened is that driven prices up substantially, you know, double digit, uh, home price growth in the last couple of years, each year. And so, you know, the question is, okay, what’s going to happen. That’s going to bring more homes on the market to hopefully maybe stabilize prices a little bit, give more opportunity, more options for buyers. And, uh, you know, if, if you’ve heard you probably, you may have been, if you follow the housing market at all, you’ve probably heard the narrative that we’re going to have foreclosures, and we’re going to have homes that were in this forbearance program that are going to come flooding on the market.

Tego:

Well, I, I’m here to tell you and I, and I’m very confident in this. That is not going to happen. There’s maybe some, but it’s not going to be a flood. One of the reasons for that is we, we know, as of today, we’re here in November of 2021. Most of the programs where people were in this for forbearance programs, uh, expired in October now that, you know, September, October, October was when a lot of them were coming up. And if there were a lot of people that were in a, in a situation where they couldn’t, you know, pick up and start making their mortgage payment again, that’s how you come out of the forbearance plan. Um, we would have seen, you know, a bunch of homes coming on the market. We haven’t seen it locally, and we haven’t seen it national

Tracy:

What’s really gone on with homes on the market. Well,

Tego:

Give me the context or what do you know, h

Tracy:

So how many houses do we have on the market compared to last month or six months ago? Okay.

Tego:

Yeah. Thank you. To put it in perspective. So we’re down about 30% over last year, which was down from the year before, which is down, but for the board the year before, let me put it this way right now, November of 21, we’re somewhere around 950 homes in the Metro Albuquerque area, which, you know, that’s residential properties, a healthy market when they say, you know, and they talk about a balanced market or a buyer’s market, or seller’s market, a healthy market, based on the current demand we have is 4,000 homes, 5,000 homes. We’re at 950, right? Yeah. So, so it’s, there’s, you know, a lot of things going on out there, interest rates has started to come up a little bit that might actually slow things down. Maybe, maybe not. Um, but, but the one trend in the data that I was trying to get to here the long way was when are we going to have more homes coming on the market?

Tego:

And if we look at the seasonal trends from now through probably the end of February, um, we’re going to continue, continue to have less and less homes in the market every week. Um, that, that holds true. I went back to 2013 and, and I’m sure it goes back further than that. I just didn’t need to go back any further is every year from about this point until the end of February, the following year, we see about 20% less homes on the market. Now, 2020 was an exception to that. But a 2020 is an exception to just about everything. Yeah, yeah. Which, which means from our 950, we have now, I mean, we could be down to 700 homes on the market.

Tracy:

That would be really tough

Tego:

It would be, and it’s, it’s unfortunate because there’s people that want to buy. We know that there’s thousands of people in our market that have, um, pre-approvals, you know, to, to purchase a home mortgage applications. We know that mortgage applications have been very strong. We’ve got that data. So, uh, I don’t know. I, I, you know, it’s just, I don’t know what to make of it other than it’s it’s not great.

Tracy:

Yeah. That’s tough. So when will we see more homes on the market? Probably March, March, probably April, definitely April, may, June, because that seasonally is when we see them, but will we see 4,005,000 homes on the market? No, we’re just going to slowly inch up for our busy season next spring. Um, which means if you’re thinking of selling might be a really good time. Yeah,

Tego:

Yeah, no, I, I mean, it’s, it’s a, it’s a challenge and I know I’m kind of tongue tied here because I’m not sure what the make of it, you know, there’s housing economists and economists out there that would like to see 4% interest rate just to suppress the market just to slow down the real estate market and, and that’s, um, possible, but not likely that we’re going to see 4% interest rates anytime soon,

Tracy:

Even if it’s 4, Tego. I mean, it can’t slow. It that much right for is still phenomenally great interest rates. And we were talking quarter percent, 8% here and there, and yes, it makes a difference. But

Tego:

Let me give you this thought experiment. Okay. If you have a home and you’ve locked in a 30 year mortgage at 3% interest rate and a year or two from now mortgage rates at, for four and a half percent, how motivated are you going to be to sell your home?

Tracy:

I think people still, you know, if they need to sell and they want to sell. Okay.

Tego:

Yeah. That’s fair. No, I’ll, I’ll accept that. I’m just, I’m just wondering with these ultra low mortgage rates that people are now locked into, um, if that’s going to be a deterrent for people putting their homes on the market in, in the future,

Tracy:

It could be. And probably Eddie would know that the lot of times what we’re seeing now is when people are buying their dream home or they’re moving up or they’re changing homes, they’re keeping their current home as a rental. So they’ve got a house that’s, you know, a great rental and you’re at a 3% mortgage might just make sense to keep that house. When you buy your other house,

Tego:

You just hit on another thing that’s that is also affecting the, the lack of supply of homes in, in the country is a lot of people are doing that. A lot of people own a second home rental home investment property, way more than, than, uh, any time in the past, right. That’s keeping homes off the market, or at least for the, for sale market. Yeah.

Tracy:

We’ve had plenty of, uh, home sellers that have chosen to keep their home and buy a new home as their primary residence.

![Your Journey to Homeownership [INFOGRAPHIC]](https://files.simplifyingthemarket.com/wp-content/uploads/2021/11/18120442/20211119-KCM-Share-549x300.png)

![Your Journey to Homeownership [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/11/18120443/20211119-MEM.png)