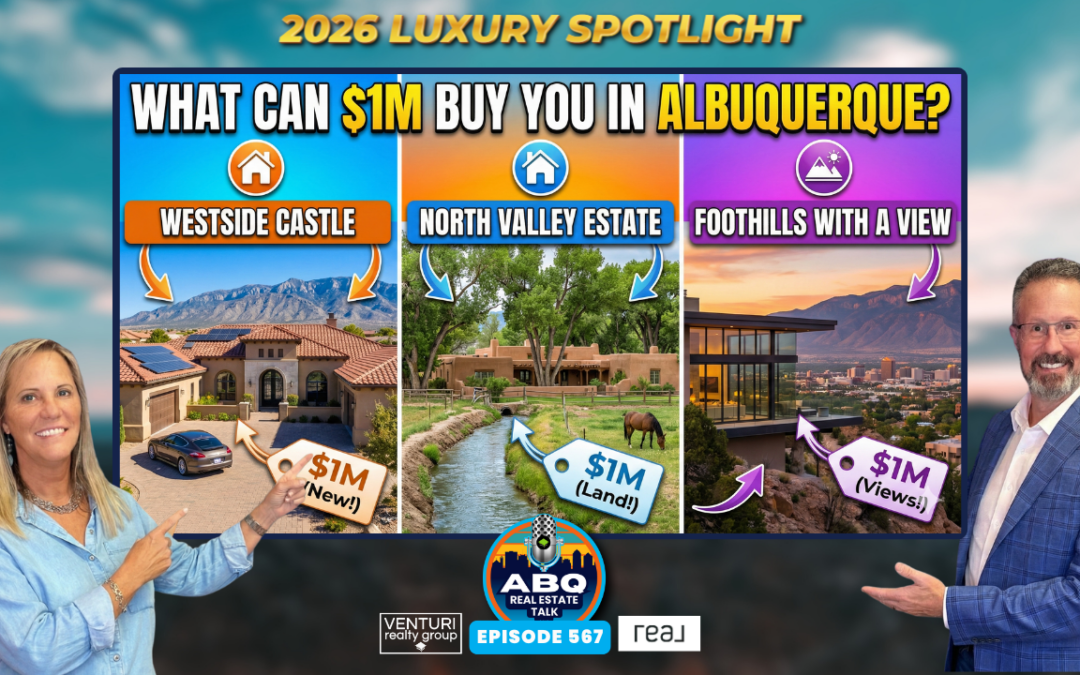

What $1 Million Really Buys in the Albuquerque Luxury Home Market

ABQ Luxury Homes: What $1 Million Really Buys in the Albuquerque Area

By Venturi Realty Group

Albuquerque Real Estate Talk – Episode 567, January 2026 Luxury Market Segment

In this episode of Albuquerque Real Estate Talk, Tego and Tracy Venturi zoom in on one thing: true luxury homes in and around Albuquerque, and what a million dollars actually buys here versus in other markets. They start by defining “luxury” the way analysts do—by looking at the top slice of real, closed sales—not just list prices or online estimates.

Using 2025 sales data, Tego explains that luxury in our market begins roughly at the top 10% of homes sold by price, which puts the threshold around $650,000. The top 5% cluster closer to $800,000, and homes at $1 million and above make up only about 2% of all sales. The top 1%—roughly 100 homes sold in 2025—start around $1.3 million. That narrow slice is where you find Albuquerque’s most exclusive properties, from gated golf-course estates and North Valley compounds to dramatic East Mountain and Placitas view homes.

“We’re talking big variety all over luxury house, the metro Albuquerque area.”

Tracy brings the perspective of a luxury-certified broker—someone who had to qualify by consistently selling homes above the locally defined luxury price point. From that vantage point, she and Tego walk listeners through luxury pockets across the metro: the Far Northeast Heights and High Desert, Corrales and the North Valley, Rio Rancho estates, Los Lunas near the Facebook data center, classic neighborhoods near UNM and Old Town, and acreage properties in the East Mountains.

“So there’s a general rule that luxury is considered the top 10% of homes sold by price in a market.”

— Tego Venturi

How Albuquerque Defines Luxury: From Top 10% to Top 1%

Instead of picking an arbitrary number, Tego grounds the definition of “luxury” in actual sales. Looking at the homes that closed in 2025, the top 10% of sales by price fall at about $650,000 and above. That’s the starting line for luxury in the Albuquerque area, not a national rule of thumb pulled from a different market.

From there, the numbers narrow quickly. The top 5% of homes sold come in closer to $800,000. A million-dollar purchase falls into a rarified group of sales—roughly 2% of all homes that closed last year. Push higher to $1.3 million and above and you’ve entered the top 1%, a tiny pool of roughly 100 sales spread across the metro’s most sought-after locations.

“A million and above, it’s about 2% of all the homes that sold.”

Tracy and Tego also emphasize that price alone doesn’t tell the full luxury story. A nearly million-dollar home on smaller acreage with ultra-high-end finishes can be just as “luxury” as a larger home on more land that’s more modestly finished. Neighborhood character, architecture, lot size, and lifestyle amenities—country club access, walkability, or dramatic views—are all part of what makes a property feel and live like luxury.

Even so, the data paints a clear pattern: the densest clusters of luxury homes are in the Far Northeast Heights and the North Valley/Corrales area. But the big takeaway from the episode is that luxury is not boxed into just a couple of ZIP codes—it’s scattered “all over the city,” from foothills to river valley to surrounding communities.

“1% would be 1.3 million. So, so if a home was purchased for 1.3 million or more, that’s the top 1% of all homes that sold.”

— Tego Venturi

Key Numbers in Albuquerque’s Luxury Home Market

- Luxury starts around $650,000 Based on 2025 closed sales, the top 10% of homes by price in the Albuquerque area begin at roughly $650,000, which is where the local luxury segment effectively starts.

- Top 5% cluster near $800,000 Homes in roughly the top 5% of the market trend closer to $800,000, marking a higher tier of price and finish within Albuquerque luxury.

- Million-dollar homes are about 2% of sales Properties at $1,000,000 and above represent only about 2% of all homes sold in the Albuquerque area in 2025, making them a relatively small but important slice of the market.

- Top 1% begins near $1.3 million The cut-off for the top 1% of sales sits around $1.3 million, with approximately 100 homes at or above that price point closing in 2025.

- Luxury is concentrated—but not confined—to key areas The Far Northeast Heights and North Valley/Corrales show the highest densities of luxury homes, yet million-dollar and near-million-dollar properties also appear in Rio Rancho, Placitas, Los Lunas, the East Mountains, and classic in-town neighborhoods.

- Finishes and lifestyle matter as much as price Tego and Tracy note that high-end finishes, neighborhood character, and lifestyle amenities—like golf, views, or large acreage—are essential parts of how buyers experience “luxury,” beyond the raw sale price.

Neighborhood-by-Neighborhood: What $1 Million Buys Across the Metro

To make the numbers real, Tracy and Tego walk through concrete examples of recent sales around the million-dollar mark. In Tanoan in the Far Northeast Heights, they highlight a home of about 4,200 square feet that sold around $1.1 million—set in a gated country-club community where residents can opt into golf, tennis, and swimming memberships and enjoy that classic “golf-cart lifestyle.”

Still in the foothills, High Desert and the Sandia Heights area showcase a different version of luxury: estate-size lots, big sky and mountain views, dark-sky-friendly lighting, native landscaping, and strict building envelopes that preserve open space and wildlife corridors. In much of this area, you can’t fence your whole lot—courtyards and limited enclosures are used instead so deer and other wildlife can move naturally through the neighborhood.

North of town in Placitas, a million-dollar home delivers what Tracy calls a Georgia O’Keeffe or Santa Fe vibe: open rolling hills dotted with chamisa, big views, and a quieter, retreat-like feel, often on larger lots that are still close enough in to keep the drive manageable.

“We’ve got something for everybody in the Albuquerque area.”

River, Valley, and In-Town Classics

In the North Valley, they point to Lee Acres off Solar Road—one of the area’s classic neighborhoods—where a roughly 3,500-square-foot home sold in the $975,000 range after extensive updating. Older ranch-style properties there have become high-end addresses thanks to mature trees, Bosque access, and proximity to the Rio Grande. Another nearby infill project, brand-new construction around $1.2 million and about 2,500 square feet, shows how new luxury can tuck into long-established pockets of the valley.

Closer to downtown, the Old Town and Albuquerque Country Club area offers million-dollar homes with a different flavor. Tracy describes a 3,700-square-foot, U-shaped New Mexico–style ranch with a courtyard—a hacienda-like layout wrapped around an interior outdoor space. It’s a blend of historic neighborhood character and updated luxury finishes just minutes from dining, museums, and the river trail system.

In Ridgecrest near UNM and Kirtland Air Force Base, a sale just under $1 million delivered walkable access to events, sporting venues, hospitals, and major employment centers. For buyers who value in-town convenience and classic mid-century neighborhoods, that kind of location is its own luxury amenity.

“Million dollars there got ’em a 3,700 square foot updated ranch style kind of… where there’s kind of the center courtyard.”

— Tracy Venturi

Rio Rancho, Los Lunas, and the Westside Bluffs

On the west side of the river, today’s luxury isn’t limited to older, in-town neighborhoods. South Rio Rancho’s Unit 10, just west of Rust Medical Center, has become a true estate area where owners buy their own lots, hire custom builders, and end up with half-acre properties. One example the team cites: a roughly 3,168-square-foot custom home around $1.05 million, loaded with high-end finishes and contemporary features.

Farther south, Los Lunas has surprised many as an emerging luxury pocket. Right across from the Facebook data center, a home around $1.1 million stood out for its “extraordinary finishes and detail”—a lot of house for the money in an area where most nearby new homes are priced in the $300,000s to $500,000s. It’s a sharp example of how a single standout property can reset expectations for what’s possible in a submarket.

Meanwhile, above the Westside bluffs near the volcano escarpments, new construction has pushed up into modern-style homes with the “latest and greatest” finishes and features. The team highlights a roughly 3,600-square-foot new build in this area at about a million dollars, illustrating how buyers can get contemporary design and big views without leaving the city’s west side.

East Mountains and Acreage Estates

Head east over the pass and luxury takes the shape of space, privacy, and views. In Paa-Ko, buyers get access to a golf course and clubhouse on lots that are typically an acre or larger, with some as big as seven acres depending on how the land was platted. Tracy notes her own history selling land in nearby San Pedro Creek Estates, where 10-acre sites and custom homes create a true mountain-estate feel.

Even farther south along the backside of the Manzanos, a 2,500-square-foot home at roughly $1 million sat on 15 acres off what locals still remember as “South 14,” now NM-337—a winding road popular with cyclists and motorcyclists for its scenery. Here, the luxury is an expansive custom home plus a 15-acre estate, trading some convenience for land and privacy that would be unattainable at this price in many larger metros.

“What a million buys here versus many of our big markets around the country… they’re just blown away.”

By the end of the segment, the message is consistent: whether you want a gated golf-course lifestyle, an updated in-town classic, a modern Westside new build, or a 15-acre mountain retreat, the Albuquerque area offers a wide range of true luxury options. Compared with many coastal and big-city markets, fellow real estate professionals are “blown away” by just how much home—and land—local buyers can secure for around a million dollars.

Frequently Asked Questions

What price range is considered “luxury” in the Albuquerque area?

In this episode, Tego defines luxury using actual 2025 sales data. The top 10% of homes sold by price start around $650,000, which is the practical entry point for the local luxury market. The top 5% cluster closer to $800,000. Homes at $1 million and above make up about 2% of all sales, and the top 1% begins around $1.3 million.

How common are million-dollar home sales in Albuquerque?

Million-dollar transactions are relatively rare. Tego notes that properties at or above $1,000,000 account for roughly 2% of all area home sales. The very top of the market—the top 1%—starts around $1.3 million and represents only about 100 sales across the entire metro in 2025.

Which areas have the highest concentration of luxury homes?

The Far Northeast Heights and the North Valley/Corrales area show the highest concentration of luxury properties when you look at density. Tanoan, High Desert, Sandia Heights, and North Valley neighborhoods like Lee Acres and Los Ranchos all feature prominently. At the same time, Tracy and Tego emphasize that luxury homes also appear in Rio Rancho, Placitas, Los Lunas, the Westside bluffs, the East Mountains, and in-town neighborhoods near UNM and Old Town.

What does $1 million typically buy in Albuquerque compared to bigger markets?

In Albuquerque, around a million dollars can buy a 4,000-plus-square-foot home in a gated country-club community like Tanoan, a fully renovated 3,500-square-foot North Valley ranch, a new-construction modern home of roughly 3,600 square feet on the Westside bluffs, or even a custom home on 10 to 15 acres in the East Mountains. Tracy and Tego mention that colleagues from larger markets are often “blown away” by how much house—and land—local buyers can get for that price.

Are there luxury options outside the Albuquerque city limits?

Yes. The episode highlights multiple examples beyond the city proper: Placitas with its open hills and Santa Fe–style views, Rio Rancho’s Unit 10 custom estates, Los Lunas near the Facebook data center with high-end new construction, and East Mountain communities like Paa-Ko and San Pedro Creek Estates where buyers can find acre-plus and 10-acre sites. All of these areas regularly see homes in the high-end and million-dollar ranges.

Have questions about Albuquerque real estate?

If you are thinking about buying or selling, or just want to understand how the current market affects your plans, our team is here to be a resource.

Call or text: (505) 448-8888

Email: info@welcomehomeabq.com

Website: WelcomeHomeABQ.com

Venturi Realty Group of Real Broker, LLC

")

")