There are many headlines about how housing affordability is declining. The headlines are correct: it’s less affordable to purchase a home today than it was a year ago. However, it’s important to give this trend context. Is it less expensive to buy a house today than it was in 2005? What about 1995? What happens if we go all the way back to 1985? Or even 1975?

Obviously, the price of a home has appreciated dramatically over the last 45 years. So have the prices of milk, bread, and just about every other consumable. Prices rise over time – we know it as inflation.

However, when we look at housing, price is just one component that makes up the monthly cost of the home. Another key factor is the mortgage rate at the time of purchase.

Let’s look back at the cost of a home over the last five decades and adjust it for inflation by converting that cost to 2021 dollars. Here’s the methodology for each data point of the table below:

Mortgage Amount: Take the median sales price at the end of the second quarter of each year as reported by the Fed and assume that the buyer made a 10% down payment.

P&I: Use a mortgage calculator to determine the monthly principal and interest on the loan.

In 2021 Dollars: Use an inflation calculator to determine what each payment would be when adjusted for inflation. Green means the homes were less expensive than today. Red means they were more expensive.

As the chart shows, when adjusted for inflation, there were only two times in the last 45 years that it was less expensive to own a home than it is today.

Last year: Prices saw strong appreciation over the last year and mortgage rates have remained relatively flat. Therefore, affordability weakened.

2010: Home values plummeted after the housing crash 15 years ago. One-third of all sales were distressed properties (foreclosures or short sales). They sold at major discounts and negatively impacted the value of surrounding homes – of course homes were more affordable then.

At every other point, even in 1975, it was more expensive to buy a home than it is today.

Bottom Line

If you want to buy a home, don’t let the headlines about affordability discourage you. You can’t get the deal your friend got last year, but you will get a better deal than your parents did 20 years ago and your grandparents did 40 years ago.

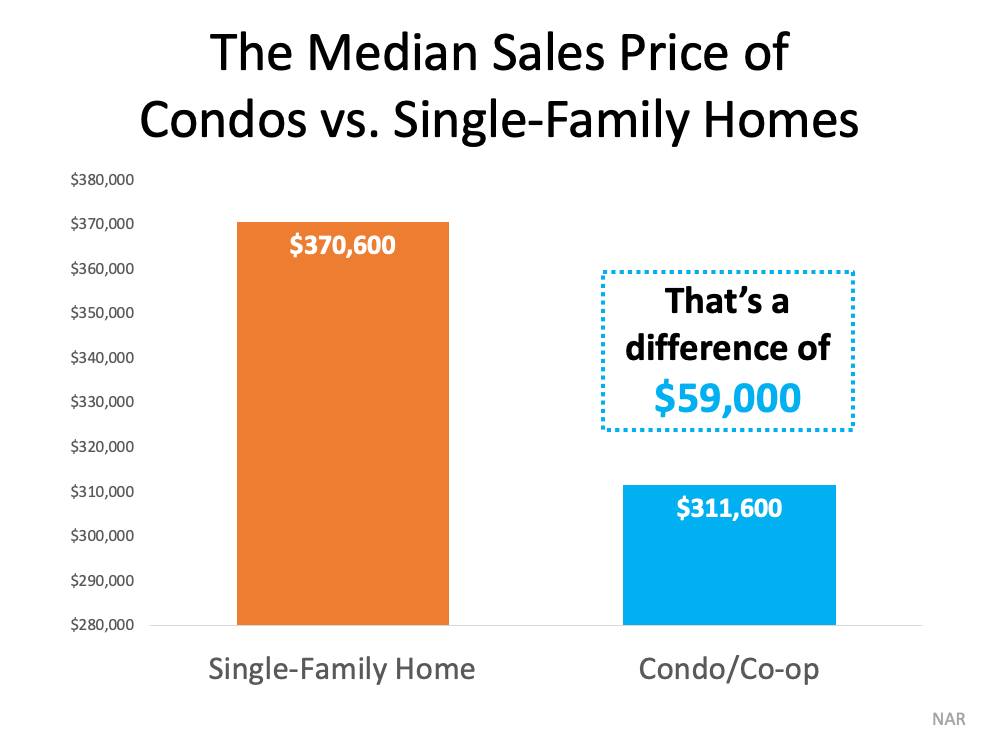

It’s no secret that one of the top stories in today’s real estate market is low housing supply and high buyer demand. If you’re a first-time buyer looking for a starter home or are someone who’s interested in downsizing, it may be worth considering a condominium (condo) as a worthwhile option.

In fact, trends indicate condos are gaining popularity among buyers. In the latest Existing Homes Sales Report from the National Association of Realtors (NAR), the data shows condo sales rising throughout the first half of this year (see graph below):There are a few reasons more and more people are opting to buy condos – the benefits of condo life can be quite compelling. Let’s explore the main perks to find out if a condo is a good fit for you.

Affordability

According to the NAR report, the median sales price of a condo is roughly $59,000 less than the median price of a single-family detached home (see graph below). This makes condos a great option for first-time homebuyers, those with limited down payment savings, or those looking to save money by downsizing.

Maintenance

A recent article from BankRate adds low maintenance as another perk of a condo lifestyle. Generally, exterior maintenance for condos is handled by a Homeowner’s Association (HOA). This can include things like landscaping and upholding a certain standard of cleanliness and condition for walkways, siding, and roofs. If you’re looking for a lower-maintenance option or see the appeal in being hands-off with upkeep, condos may be a good choice for you. With exterior maintenance off your plate, you’ll have more time for yourself and your hobbies.

Amenities

You can use that free time to enjoy some of the value-adding features your condo community may have, which could include dog parks, pools, a rentable clubhouse and grilling area for events, and more. If being able to host or attend community social outings is important to you, condos may give you more opportunities to enjoy the company of your neighbors. As a bonus, some condos even have gyms and on-site security teams.

Ultimately, the choice is yours. Condos are great options that often come with various features and benefits that may be important for your lifestyle. Fannie Mae sums up the appeal nicely:

“Condominiums, or condos, can be great alternatives to detached homes. City dwellers, singles, couples, seniors, and many others may find condos that suit their needs and budgets. Others may simply prefer low-maintenance living. Buyers who feel ‘priced out’ of homes may discover condos offer an affordable homeownership alternative.”

Bottom Line

If you’re looking for a home, it may be time to consider a condo as an option. Let’s connect to explore if one would be a good fit for your homeownership needs.

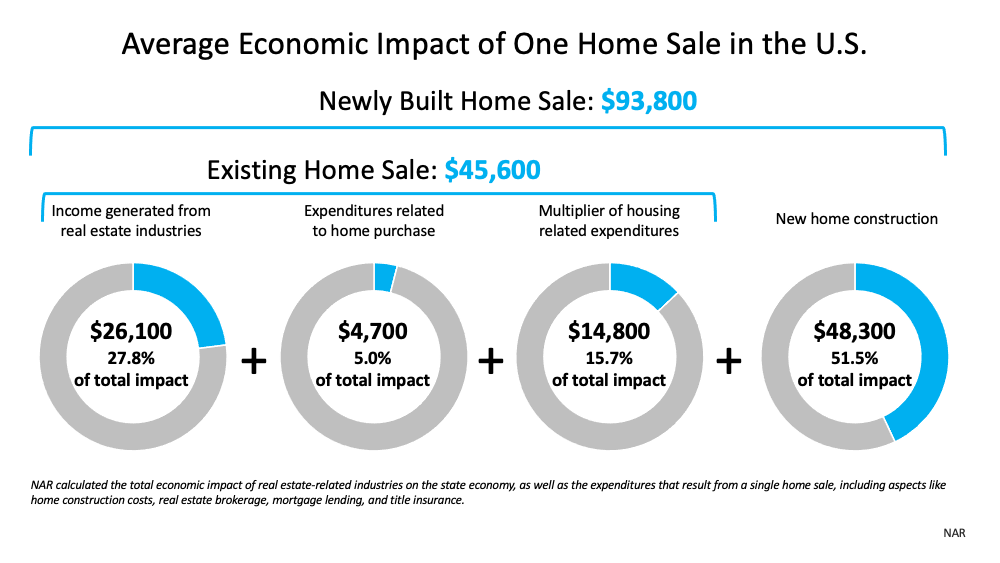

If you’re thinking of buying or selling a house, chances are you’re focusing on the many extraordinary ways it’ll change your life. What you may not realize is that decision impacts people’s lives far beyond your own. Home purchases and sales are significant drivers of economic activity. They have a major impact on your community and the entire U.S. economy via the multiple industries and professionals that take part in the process.

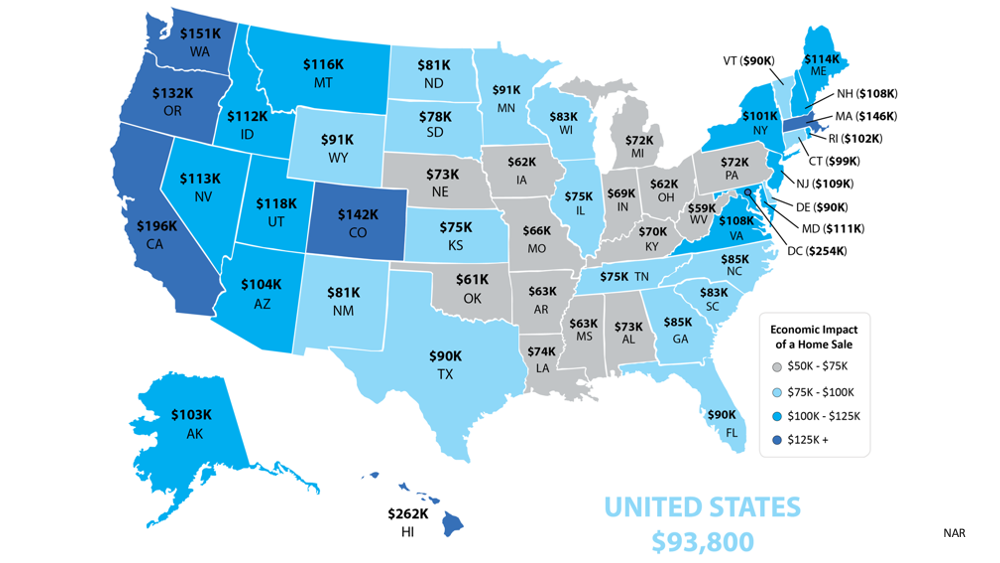

The National Association of Realtors (NAR) releases a report each year that highlights just how much economic activity a home sale generates. The chart below shows how the sale of both a newly built home and an existing home impact the economy:To dive a level deeper, NAR also provides a detailed look at how that varies state-by-state for newly-built homes (see map below):As you can see, a single home sale can have a massive effect on the overall economy. Ali Wolf, Chief Economist for Zonda, talks about this in a recent article, noting there’s a significant impact at each distinct phase of the transaction:

“The housing market contributes to the economy in four main stages: during planning and land development, throughout the actual construction of the home, at the point of sale, and upon moving in.”

When you buy or sell a home, you’re leaving a lasting impression on the community at large in addition to fulfilling your own needs. That’s because each stage of the process involves numerous contractors, specialists, lawyers, town and city officials, and so many other professionals. Every individual you work with, from your trusted real estate advisor to the architects who design new homes, has their own team of professionals involved behind the scenes.

Bottom Line

Homebuyers and sellers are economic drivers in their community and beyond. If you’re thinking of buying or selling, let’s connect today to start the process. It won’t just change your life; it’ll make a powerful impact on our entire community.

Tracy. We’ve got a great story and some data here about, should you wait to buy?

Tracy:

And the answer is it could cost you if you wait to buy. Right.

Tego:

So tell us the numbers on this. This is a little bit of research. It was done. Pretty simple research, but yeah, go, go through it

Tracy:

Here. You know, it’s talking about a $250,000 home loan. So we’re looking at the price of the home versus the cost of borrowing the money from now to historical, you know, like in the future, if interest rates change and prices continue to go up, which we believe they will.

Tego:

Yeah. So if you look at, if somebody bought a home in the beginning of this year in January and they pay $250,000 for it, they got a 2.8% mortgage. So they got a month monthly payment about 1,077 a month, right? If the home prices go up, which they look like they will about 12% this year, right?

Tracy:

That home next January will be 200, $280,250. Right? So that house is going to go up $30,000 in a year. Wow. And interest rates let’s look at it this

Tego:

Way. This may be a better way to look at it. If somebody would buy a $280,000 house right now, and let’s say, they’re close, they’re there around, you know, 3% mortgage rate or something like that. They’re going to have a payment around $1,200, let’s say. Right. Okay. All the projections are that home prices are going to appreciate somewhere around 5%. I think it’s going to actually be higher than that over the next 12 months, that home let’s say it’s 5%. That home that was 280 is now worth $295,000 a year later. So if you wait a year from now, you’re going to pay another $15,000 for that exact same home. And more than likely you’re going to be paying a higher mortgage payment. So you’re going to, because your interest rates more than likely will be up a little higher by the time, the same time next year.

Tracy:

So we’ve had a lot of people say, I’m just going to wait. I’m not, I’m not going to buy a house right now. I’m just going to wait for things to calm down prices to come down or whatever. So when you look at the statistics on it and the projections that really could cost a home buyer, especially for that, that whole

Tego:

Conversation that you and I have all the time about building wealth for you and your family.

Tracy:

So, you know, this example was a January, 2021 purchase. So just six months ago, right. Seven months ago. And it’s showing that that house has already appreciated by $15,000 perhaps. And what we know from working in the market and helping clients is houses have gone up quite a bit just since the first of the year. So to wait and wait for prices to go up higher and potentially miss out on the best interest rates we’ve seen pretty much could, could cost them money.

Tego:

What about all those forbearances in that foreclosure,

Tracy:

Foreclosure flood that’s coming Tracy. So we’ve got a lot of new data on that too. Right? So over our morning, coffee, tea goes always reading the stories, right? Yeah. And the story of this week was all about what’s going to happen with all the houses in forbearance, but think about how many houses are there in forbearance, Tigo from the height of this pandemic to today. Right? Right. We went from what five, 6 million make something clear. If people may not

Tego:

Understand this, they may have heard the, hear the word for Baron. So the forbearance is a, a program that was put in place to help people avoid foreclosure. I remember back when, when it first started and everybody was saying there’s 7 million or 5 million people on a forbearance, they’re all going to go to foreclosure. Well, th the whole idea of the forbearance program was to get people to avoid foreclosure, right. It was a way to let them put a pause on their mortgage payments because of the pandemic and then come out of it. So what’s happened. We started at 5 million, we’re down to under 2 million people in those plans right now in most of the people that have come off, those plans have just, you know, picked up payments, done some work out with their lender, or they they’re there. Honestly, there were a lot of people that did the plan that never used it. They’re out of the plan. There’s a lot of people that refinanced or did something else that are out of the plan. Right.

Tracy:

So now we’ve got under 2 million people still in the forbearance plan and the story you were telling me, I think it was FHF well,

Tego:

It was actually it was a story. It was a CFPB.

Tracy:

I know, I know

Tego:

FHA is a federal housing finance authority, which oversees Fannie and Freddie, and then CFPB consumer protection. So they’re the ones that are, that are, you know, pushing you know, helping people get through this you know, homeownership challenge. Right, right.

Tracy:

So they’re coming out with how people are going to get out of it, right. How they’re going to help people, but what happens to the folks that aren’t trying to help themselves get out of it. Right. Right. And that was really clear to me that if people are reaching out to their lender, if they are in forbearance or they’re trying to figure out a path, here’s the quote they’re going to be. Let’s see. I just found it.

Tego:

So this was a story in housing wire written by a gentlemen who is with a organization called Realty track. And they’re the largest company in the country that kind of deals with foreclosures that the data foreclosures and working through foreclosure. So anyway, you know, they’ve had no business in the last year. I actually,

Tracy:

So the quote or the,

Tego:

The whole idea was okay, of all these people that were in forbearance plans. And I mean, they’re going to be coming out of it. The foreclosure moratorium is going away.

Tracy:

Probably it is like today soon. Yeah. I think it is first. I think you’re

Tego:

Right. So, so what happens to all those people now, are we going to suddenly have this flood of foreclosures? Well know, here’s, here’s the quote. It says the CFPB has issued new servicing rules. And so what the services are, those are the ones that actually take care of the mortgage payments and in service service to mortgages. So when you make your payment on a mortgage, you’re paying it to a servicer just to define that rules providing even more safety net until January, 2022, for the balance of 2021 service will not only be, we’ll only be able to initiate foreclosures on loans, held on vacant and or abandoned properties loans where the borrower has been offered, but not qualified for loan modification loans, where the borrower has been unresponsive to service our outreach. And I want to go back to that. And loans were, let’s see, which were 120 days delinquent prior to March of 2020, which is kind of funny that, you know, all those people that were prior to the pandemic got their, their foreclosures put on hold to.

Tracy:

So if they were in the process 120 days, they were, they might get put back on the roster. So

Tego:

That little part in there that says, if they’ve been, if the homeowner has been unresponsive to service or outreach the servicers, again, the people that actually handle the mortgages and collect payments and process all that they’ve been doing tons to for outreach. I mean, if you go on any mortgage servicers website right now, the first thing you’re going to see is this big splash pop up that says, do you need assistance with your mortgage? Right? This is nothing like what happened in 20 2008. Right. Anyway.

Tracy:

So basically it’s saying if you’ve been trying and you’re cooperating and you’re communicating with whoever you pay your mortgage to, they’re not going to start a foreclosure there. They’re going to continue to figure out how to help you put back payments. Well, there there’s one little

Tego:

Caveat to that. And it says they’ve been offered, but not qualified for loan modifications, which means the thing is they’re going to do everything they can to help people modify their mortgage. If they need to it’s as much as putting all the payments, the end and making it a 40 year mortgage. Right.

Tracy:

We saw that we had to do the math 480 months. Yeah.

Tego:

So the, the end of this story is Tracy. There’s not going to be a flood of foreclosures.

Tracy:

No, there isn’t. And you know, with under 2 million people in a forbearance, even if all those came on the market, we probably need them on the market. Not that we want that to happen. If they

Tego:

All came on the market and they wouldn’t come on all at once, they would come in over

Tracy:

The next year or two. Yeah. The

Tego:

Projection I saw was maybe 300,000 foreclosures nationwide after we get through this forbearance. And everybody comes off of that nationwide. Really? That’s a drop in the bucket. When you think about the fact that there’s about 6 million homes a year sold in our country,

Tracy:

The other statistic, just to put it in perspective is of the, the under 2 million that are in the forbearance program represents about 3.9% of mortgages. Right? So that’s four out of a hundred.

Tego:

So even if all those what I want. Yeah, you’re right. No, the thing is, even if all those homes come on the market immediately, it’s not going to cause price, declines and less buyer demand, just vanishes for some crazy reason, which doesn’t seem to be in the cards with the millennial

Tracy:

General and think about how much home prices have changed since the beginning of last year. Those, those people in forbearance have equity in those homes. So

Tego:

Or discussion we wanted. But I I’m just so frustrated when I hear people say, well, I’m waiting for the deals. When all the deals start coming, it’s like, no, they’re not coming. They’re they’re not, I’m sorry. And people that say you shouldn’t be telling people to buy a home right now because home prices are going to crash. Well, first off you gotta live somewhere. Right. I mean, so you got to put that into the calculation anyway. Okay.

If you’re thinking of selling your house but don’t know what you should buy, you have options.

Existing homes offer a wide variety of home styles, an established neighborhood, and lived-in charm. Meanwhile, new home construction lets you create your perfect home, cash in on energy efficiency, and minimize repairs.

Whether you’re looking for newly built or existing homes, both have their perks. If you’re ready to sell your house, let’s connect today to go over the perks of both existing and newly built homes to find out what’s right for you.

As the chart shows, when adjusted for inflation, there were only two times in the last 45 years that it was less expensive to own a home than it is today.

As the chart shows, when adjusted for inflation, there were only two times in the last 45 years that it was less expensive to own a home than it is today.

![Ready To Sell, but Don’t Know Where You’ll Go? [INFOGRAPHIC]](https://files.simplifyingthemarket.com/wp-content/uploads/2021/08/05134513/20210806-KCM-Share-549x300.png)

![Ready To Sell, but Don’t Know Where You’ll Go? [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/08/05134515/20210806-MEM.png)